Public and private energy companies should address year-end 2019 goodwill and long-lived asset impairment testing procedures so quarterly and financial audits and reviews can go smoothly and allow for greater transparency.

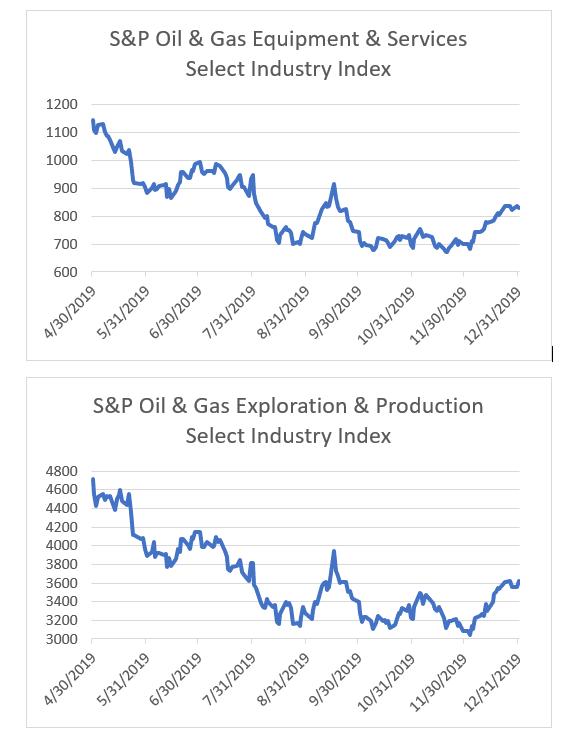

Market equity prices and indices continued to decrease for many energy companies during 2019. For instance, between April 30, 2019 and December 31, 2019, the S&P Oil & Gas Equipment and Services Index decreased by approximately 27 percent, inclusive of a rebound in the fourth quarter. Likewise, the S&P Oil & Gas Exploration and Production Index decreased by 23 percent during this same timeframe, also inclusive of a slight rebound in the fourth quarter.

With the continued decrease in market capitalizations, coupled with commodity price declines in recent years, auditors and regulators will continue to have a renewed focus on impairment testing for goodwill and long-lived assets on the balance sheets of energy-focused companies.

Under Accounting Standards Codification Topic 350, Intangibles: Goodwill and Other (ASC 350), goodwill is tested for impairment at least annually or when a triggering event dictates. For more information about how amendments to ASC 350 in 2017 simplified the process of testing goodwill for impairments, CLICK HERE.

Under Accounting Standards Codification Topic 360, Property, Plant and Equipment (ASC 360), long-lived assets are tested for impairment when a triggering event dictates. Continued declines in market prices such as those that occurred during most of 2019, along with associated changes in industry fundamentals (e.g., changes in drilling plans for E&P companies and changes in customer buying patterns for oilfield services companies), may qualify as a triggering event.

Publicly- and privately-held companies need to adequately address their year-end 2019 goodwill and long-lived asset impairment testing procedures. Doing so in a timely manner will ensure that year-end and quarterly financial statement audits and reviews will proceed as smoothly as possible, as well as allow for greater shareholder and stakeholder transparency.

Kevin Cannon is a Principal in Opportune’s Valuation practice based in Houston. He has 19 years of experience performing business and asset valuations and providing corporate finance consulting. His specific experience includes valuations of businesses and intangible assets for purchase price allocations, impairment, tax planning, management planning and portfolio valuation purposes for companies in a variety of industries, including oil and gas, oilfield services, and industrial manufacturing.

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

- Kevin Cannonhttps://oilmanmagazine.com/author/kevin-cannon/

Oil and gas operations are commonly found in remote locations far from company headquarters. Now, it's possible to monitor pump operations, collate and analyze seismic data, and track employees around the world from almost anywhere. Whether employees are in the office or in the field, the internet and related applications enable a greater multidirectional flow of information – and control – than ever before.