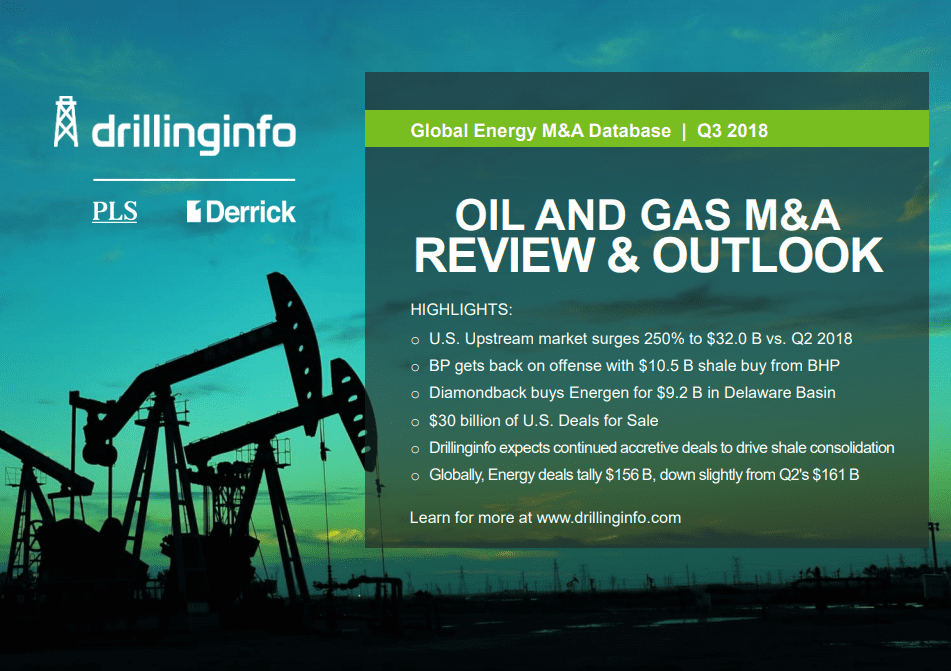

Austin, TX – Drillinginfo, the leading energy SaaS and data analytics company, reports that U.S. oil & gas M&A activity in Q3 2018 surged 250% over Q2 and broke all quarterly records dating back to Q4 2012. The final tally for Q3 is $32 billion, up from $9.1 billion in Q2.

As Drillinginfo correctly predicted at the beginning of July 2018, factors that led to the dramatic increase include:

- More than $50 billion of deals for sale as of July 1 largely by motivated sellers.

- More than $15 billion of private equity dry powder looking for rapid deployment.

- Mandates by Wall Street for public companies to focus on core-of-core to drive free cash flow.

- Elimination of the sub-$50 oil price risk with stable to higher pricing on the horizon.

- Consensus view of stable to higher oil prices.

In a soon-to-be-released report, Drillinginfo findings show $32 billion in activity during 3Q 2018 which is 76% above the quarterly average of $18.3 billion dating back to 2009. The highlight of the quarter was BP’s $10.5 billion strike to buy a portion of BHP’s U.S. onshore portfolio (Permian, Eagle Ford and Haynesville) which is the single largest asset level purchase on record and also marks BP’s return to offense with its largest upstream buy since buying ARCO for $28 billion in April 1999. BP reportedly beat out Shell for this asset package – a dynamic that solidifies the importance of the U.S. shales as a key portfolio element for global majors. Also during Q3, Permian-focused Diamondback Energy boldly acquired fellow-Permian producer Energen Resources for $9.2 billion – a number just shy of the Permian record $9.5 billion paid by Concho Resources for RSP Permian during Q1 2018.

“We expect U.S. M&A activity to continue at a heightened level,” said Drillinginfo Senior Director Brian Lidsky. “The industry is regularly reporting record well results across the U.S. shales as it continues to de-risk acreage positions and advance technology,” he said.

“As Wall Street is increasingly discriminating among public companies, the food chain of the big getting bigger is alive and well – shale basin leaders are being rewarded for mastering scale, efficiency and technology. This sets the stage for additional mergers that not only checks all the accretive boxes for the buyer, but also provides sellers upside by joining forces with these leaders,” said Lidsky.

“We view the recent Concho and Diamondback examples in the Permian as the start of a trend – not one-off style hits. Shale basin consolidation will be a continuing theme supplemented by occasional major new entrants for those few large and global companies who have not yet established a significant shale presence. Private equity and private companies will continue to play a role in deploying carefully calculated risk dollars to fringe areas and benches within established resource plays plus advancing today’s technology to new areas like the Powder River Basin as well providing inventory as they move to divest mode,” said Lidsky.

Loading...

Loading...

Top Takeaways from Q3 2018 U.S. M&A:

- Activity catapulted to $32 billion versus $9.1 billion in Q2 and $18.2 billion quarterly average since 2009 and is the highest quarter since Q4 2012’s $37.8 billion.

- Interestingly, on the first trading day of Q4 2018, near month NYMEX WTI breaches the psychologically important $75 level, settling at $75.30 (up $2.05/bbl) and the first close above $75 since November 24, 2014 (just before the latest oil price crash).

- BP won the prized onshore shale portfolio of BHP for the largest asset level U.S. deal recorded for $10.5 billion, reportedly beating Shell who likely remains on the hunt.

- Diamondback Energy buys Energen Resources in a Permian-consolidation play for $9.2 billion confirming that Q1’s Concho/RSP Permian $9.5 billion deal was not an aberration of the consolidation thesis.

- The “show me the cash” mood of Wall Street remains intact and favors larger companies that have visibility to free cash via substantial Tier 1 acreage in focused portfolios.

- An early September land auction in the New Mexico portion of the northern Delaware Basin breaks all BLM land sale records at $972 million with record high bids reaching $95,001 per acre.

- While active, the M&A market remains largely in the buyer’s camp as examples of motivated sellers failing to receive minimum acceptable bids include SandRidge Energy (attempted corporate sale) and Whiting Energy (Niobrara assets in Colorado).

- Globally, Q3 2018’s $156 billion in energy transactions across the value chain (Upstream, Midstream, Downstream, OFS, Power, Utilities, LNG) compares to $161 billion in Q2 2018.

Themes and Drivers Looking Forward:

- Expect continued high pace M&A activity in the next 6-12 months.

- $30 billion of U.S. deals for sale provide high quality inventory for deal activity.

- Consolidation within shale plays likely to increase in momentum as scale and efficiency rewards larger players.

- Private capital will be leaders in de-risking fringe areas of known plays plus deploying latest technologies to new areas like the Powder River Basin, as an example.

- Permian takeaway constraints present strategic opportunities over the next 18 months.

- Wall Street mandate for positive cash flow is favoring larger companies from an equity valuation perspective as acreage positions in Tier 1 areas provide strong visibility.

- The energy sector of the S&P 500 remains under-represented from a historical viewpoint and upside exists driven by higher oil prices as well an inflation hedge.

Gas asset transactions generally restricted to de-risked and economically viable development assuming $3.00/gas with proximity to growing Gulf Coast LNG and Petrochemical demand playing a factor.

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

Oil and gas operations are commonly found in remote locations far from company headquarters. Now, it's possible to monitor pump operations, collate and analyze seismic data, and track employees around the world from almost anywhere. Whether employees are in the office or in the field, the internet and related applications enable a greater multidirectional flow of information – and control – than ever before.