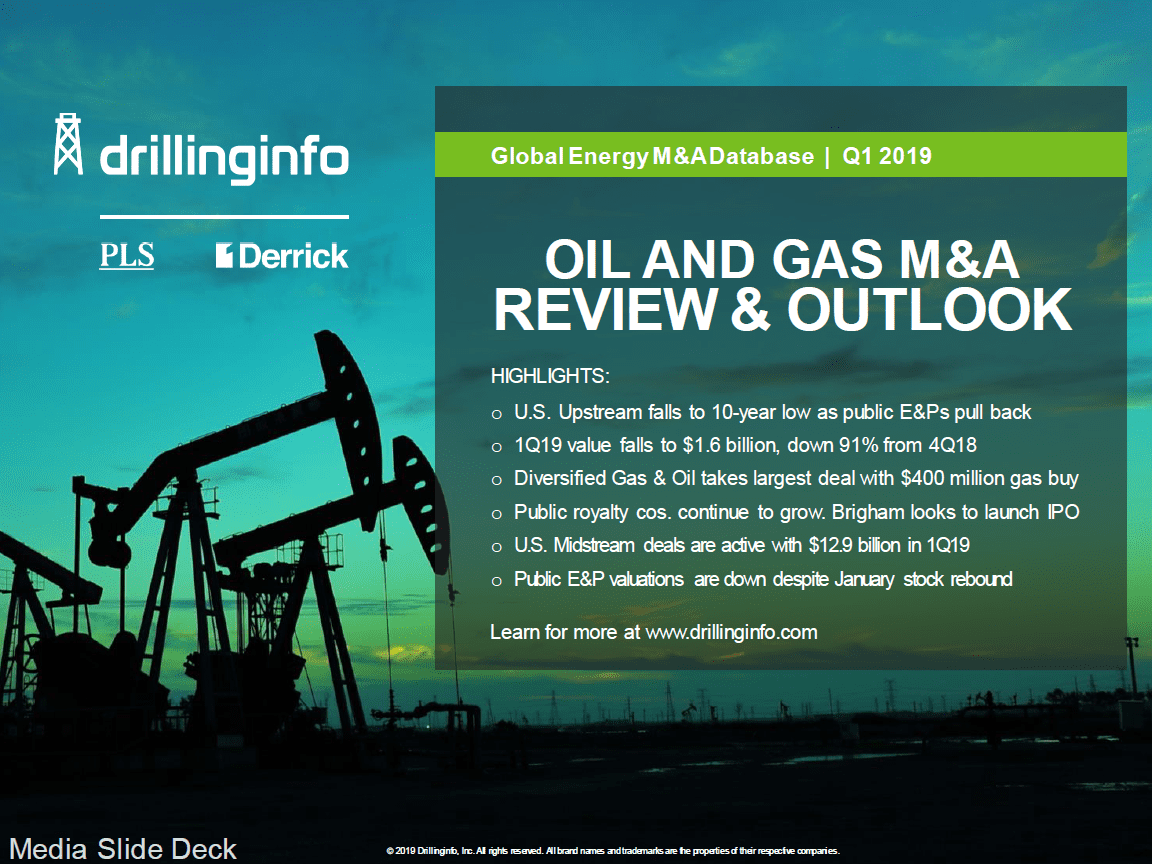

Austin, Texas – Drillinginfo, the leading energy SaaS and data analytics company, reported today that U.S. oil and gas M&A deal values have plunged to a record 10-year low in the first quarter of 2019. A slump that began in late 2018 has carried over into the new year and the $1.6 billion in Q1 deals is down 91 percent from Q4 2018, and down 93 percent compared to Q1 2018. The slump follows the $82 billion in deals in 2018 that set a four-year record high.

“The market for upstream deals came to a halt in late 2018 with the combined pullback in oil prices and equities,” said Drillinginfo M&A Analyst Andrew Dittmar. “Since then, oil has rebounded by 20 percent and E&P stocks are up 15 percent, albeit with nearly all those stock price gains taking place in early January. However, deals haven’t returned in a meaningful way and we believe that is being largely driven by Wall Street,” said Dittmar.

Remaining consistent with Drillinginfo analysts predictions at the start of the year, a confluence of factors drove deal values down, including the rapid 40 percent drop in oil prices in late 2018. The primary contributing factor appears to be Wall Street’s pressure to deliver on free cash flow and weak equity and debt markets available to fund deals. Meanwhile, private equity – which has in recent cycles stepped in as an opportunistic buyer to take advantage of pullbacks by public E&Ps – has largely sat on the sidelines.

The Drillinginfo analysts continued by highlighting that the lack of buying enthusiasm appears to be changing the game plan for would-be sellers. While there are significant assets for sale, perhaps most notably BP’s major push to sell non-core U.S. properties, some companies are using “soft” marketing processes that only reach out to a few, select potential buyers. This is particularly true for private equity-backed E&Ps, which have historically been selective in choosing their entry and exit points. While some smaller positions may be sold or merged into larger portfolio companies, these firms have no intention to give away their prime positions in major plays during a down market. The inflection point, when positive, sustainable free cash flow is reached, remains the key for the U.S. shale business.

“Having just concluded Q4 2018 earnings and announcing 2019 playbooks, most operators pivoted strategies to appease Wall Street including throttling back on growth and capex to focus on moving sustainable free cash flow forward,” added Drillinginfo Senior Director Brian Lidsky. “In theory, the current struggles of smaller E&Ps sets the stage for consolidation, with larger players able to leverage premium valuations and operating efficiencies to acquire smaller competitors. Whether these operators will step up remains to be seen,” said Lidsky.

Drillinginfo analysts pointed to another potential outcome that could involve private capital coming forward as a buyer of public E&Ps – if they see distressed valuation opportunities, as was seen earlier in the year with Elliott’s currently unaccepted $2.55 billion (including debt) bid for QEP Resources.

Ultimately, 2019 could be a watershed year for U.S. shale. If free cash flow is reliably demonstrated, Wall Street’s approval is likely to return along with capital for deals. Given the current backlog of assets, there could be a rapid return of activity once the outlook improves.

Top Takeaways from Q1 2019:

- Total of $1.6 billion in deals in Q1 2019 is the lowest quarterly deal total in 10 years

- Diversified Gas & Oil had the largest deal with $400 million Appalachian acquisition

- One Marcellus deal makes up 25 percent of Q1 value, another 22 percent comes from conventional

- Public royalty companies continue to grow with deals by Kimbell and Viper

- Brigham Royalties looks to capitalize on enthusiasm for the royalty sector with IPO

- Majority of 2018 corporate deals did close, but Denbury/Penn Virginia pulled the plug

Outlook for Q2 2019:

- Deals are likely to remain fairly slow in the near-term but with some Q2 rebound

- Likely to be greater use of DrillCos and JVs to plug funding gaps outside of debt/equity

- Valuations on public E&Ps look cheap compared to recent A&D deals, especially among the smaller companies. Look for some public companies to be consolidated/bought out

- Struggling companies without a ready buyer may be forced to restructure, similar to 2015/16

- Remains to be seen if larger operators will act on basin consolidation despite premium equity valuations compared to smaller companies

- The pace of a comeback in the A&D markets is dependent upon a reversal of sentiment by Wall Street towards the E&P sector

Loading...

Loading...

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

- U.S. Energy Media Staffhttps://oilmanmagazine.com/author/oilmanwp/

Oil and gas operations are commonly found in remote locations far from company headquarters. Now, it's possible to monitor pump operations, collate and analyze seismic data, and track employees around the world from almost anywhere. Whether employees are in the office or in the field, the internet and related applications enable a greater multidirectional flow of information – and control – than ever before.